FHA Loans: Tiny Bubble, Huge Panic

Is the Wall Street Journal's warning about FHA loans creating another 2008-style housing crash legitimate? The surprising data shows FHA loans represent just 0.27% of the mortgage market. Get the facts before making your next move.

The Wall Street Journal publishes an opinion piece, and suddenly the financial airwaves are crackling. Headlines blare: "Subprime Mortgages Are Back!" "Housing Bubble 2.0!" "Head for the Hills!" Your phone probably hasn't stopped buzzing with dire predictions. Is it 2008 redux?

Are we teetering on the edge of another housing meltdown, the kind that might let you snag real estate for pocket change? Before you start converting your portfolio to canned goods and gold bars, let's cut through the noise and look at what's really going on.

Insights

- Current FHA loan concerns, while warranting attention, do not mirror the systemic risks that triggered the 2008 financial crisis.

- The segment of FHA loans highlighted as "problematic" represents a very small fraction of the total U.S. residential mortgage market.

- Today's housing market is underpinned by stronger lending standards, higher homeowner equity, and significant regulatory reforms post-2008.

- Rising FHA delinquencies signal stress for some borrowers but are not indicative of an imminent, widespread housing market collapse.

- Critical analysis of data, understanding scale, and focusing on fundamentals are vital to navigating sensationalized market narratives.

The Spark: Media Alarms and FHA Basics

The argument, in essence, is that relaxed underwriting standards for government-backed loans are supposedly inflating house prices and brewing a new subprime storm, with taxpayers footing the bill. The finger points squarely at FHA loans – Federal Housing Administration loans – and specifically at borrowers with debt-to-income (DTI) ratios topping 43%.

What does DTI mean? It's a straightforward calculation: all your monthly debt obligations (think mortgage, car payments, student loans, credit card minimums) divided by your gross monthly income. If you pull in $10,000 a month before taxes, a 43% DTI means your total debt payments are no more than $4,300.

Conventional mortgages typically prefer to see you at or below that 43% threshold. It’s a gauge of your ability to manage your debts if life, as it often does, throws a financial curveball – a job loss, an unexpected medical bill.

FHA loans, by design, cater to individuals who might not fit neatly into the conventional lending box. They often permit a higher DTI, sometimes exceeding 50%. And yes, borrowers can often secure these loans with as little as 3.5% down.

Are FHA loans inherently riskier than their conventional counterparts? The author of that WSJ piece isn't entirely off base here; a higher DTI, lower down payment, and sometimes lower credit scores do introduce a greater potential for default if economic conditions sour.

The argument presented is that since underwriting standards were supposedly "eased," we've seen more FHA borrowers exceeding that 43% DTI threshold. Data cited in the discussion around the WSJ piece suggested that approximately 61% of FHA buyers in 2024 fell into this category.

This isn't exactly a shocking revelation. That's often why people turn to FHA loans – because they don't meet the stricter DTI requirements for conventional financing.

Echoes of 2008? Unpacking the Comparison

Then comes the supposed knockout punch, the statistic designed to send shivers down your spine. The WSJ opinion piece highlighted figures similar to this:

"About 6.8% of FHA mortgages issued in the prior year went seriously delinquent (90 days or more past due) within 12 months."

Figures central to the WSJ Opinion Piece Argument (as reported and updated)

And the follow-up intended to invoke maximum fear:

"That’s approaching the 2009 peak of the subprime mortgage bubble of 7.2%."

Figures central to the WSJ Opinion Piece Argument (as reported and updated)

Cue the dramatic music. Any comparison to 2008 or 2009 conditions immediate anxiety. We're all conditioned to brace for the worst when those years are mentioned.

But hold your horses. Are we genuinely comparing apples to apples, or is this more like comparing a firecracker to a tactical nuclear device?

Make no mistake: FHA loans were not the primary antagonists in the 2008 financial crisis. Not even close.

The 2008 meltdown was ignited by a largely unregulated private lending market on a rampage. We had the infamous "NINJA" loans – No Income, No Job, No Assets. It sounds like a punchline now, but lenders were, with alarming frequency, throwing money at almost anyone who could fog a mirror, often using deceptive teaser interest rates that would explode upwards after an initial period.

Those were the truly toxic subprime loans. FHA loans, even during that chaotic period, maintained some level of underwriting. They verified employment. They checked credit histories. The system wasn't perfect, but it was a galaxy away from the Wild West conditions prevailing in the private-label subprime arena.

So, to draw a direct, equivalency-implying line between current FHA delinquency rates and the "2009 subprime mortgage bubble peak" is, to put it mildly, a stretch. It’s like suggesting a rise in go-kart mishaps signals an imminent Formula 1 catastrophe.

Yes, rising delinquencies in any loan category are a yellow flag. They indicate economic stress. People are finding it harder to make ends meet. That is a genuine concern. But it doesn't automatically mean FHA loans are poised to demolish the entire housing market in a repeat performance of their much more dangerous, distant cousins from 2008.

"The subprime mortgage crisis was a stark reminder that excessive risk-taking without proper oversight can have devastating consequences for the entire financial system."

Ben Bernanke Former Chairman of the Federal Reserve

The Scale of the "Threat": FHA's Real Footprint

Now, let's get to the part of the story that frequently gets lost in the dramatic headlines or buried deep in the footnotes – if it's mentioned at all.

The WSJ piece, and the alarm bells it rings, appear to paint a picture of systemic risk rooted in FHA loans. But what portion of the overall mortgage market are we actually discussing?

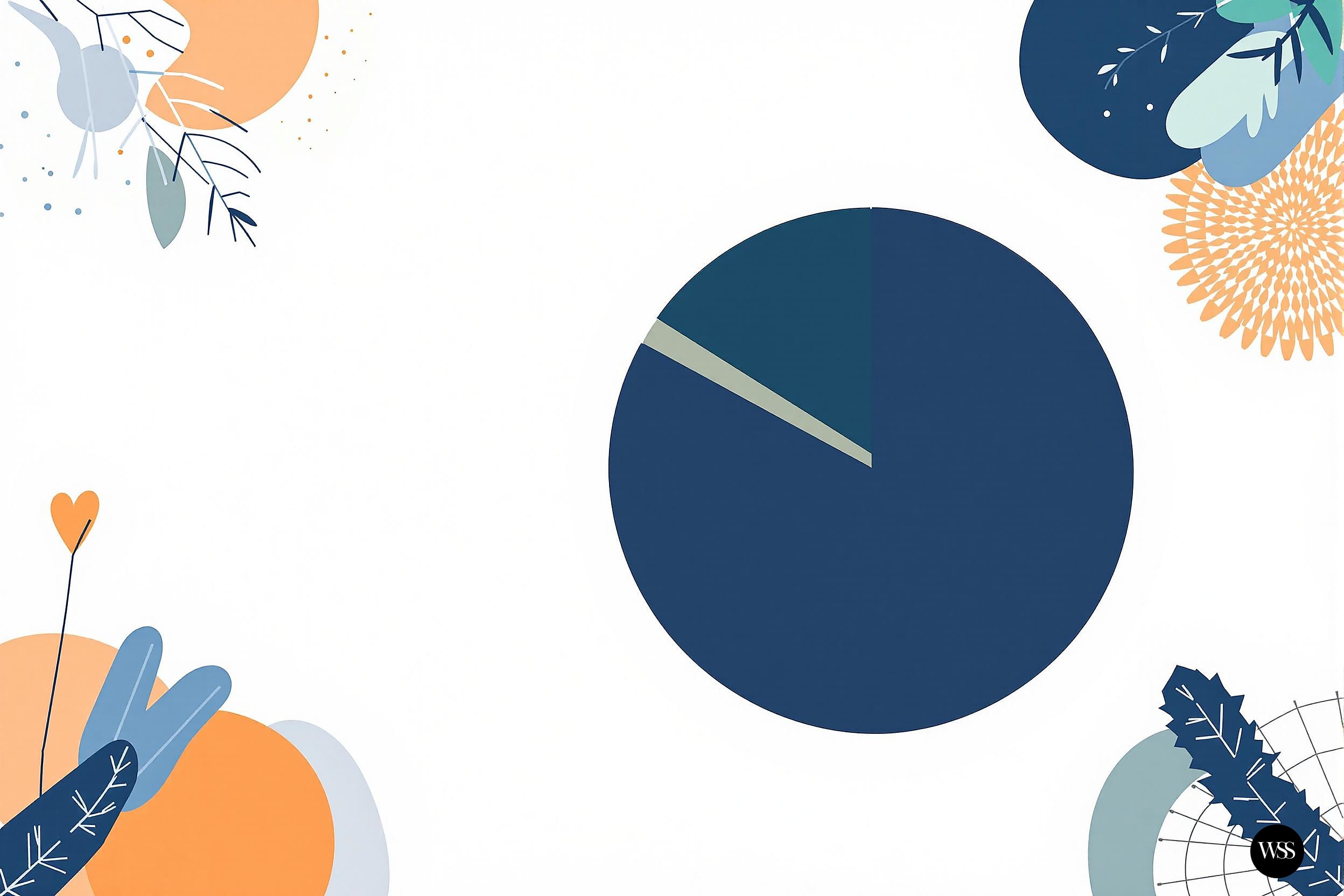

The total outstanding residential mortgage market in the U.S. is a colossal figure – around $13.9 trillion as of early 2025. That's trillion, with a 'T'.

The critique of that WSJ article, as I understand it, pointed to a specific figure of FHA debt being flagged as particularly problematic – let's use the $36 billion figure that was part of that discussion.

If you take that $36 billion, representing the supposed core of this new "subprime" threat, and compare it to the $13.9 trillion total market, what percentage do you get?

Roughly 0.26%. That's just over a quarter of one percent.

Consider that figure for a moment. An entire narrative of an impending subprime housing bubble, a repeat of 2008, is potentially being constructed from perceived issues within a segment that represents about 0.26% of the total mortgage debt outstanding in the country.

Now, are FHA loans a more significant part of new mortgage originations? Yes. They account for approximately 12% of new purchase loan dollar volume as of 2024-2025. That's not trivial for new homebuyers.

But the idea that the existing FHA portfolio, or even a stressed portion of it as highlighted by the WSJ's alarmist tone, is going to trigger a systemic collapse on the scale of 2008 based on that tiny fraction of total debt? That requires a substantial leap of logic, and perhaps a suspension of disbelief.

It's an overreaction, somewhat like finding a flickering lightbulb in your house and concluding the entire national power grid is on the verge of collapse.

Today’s Fortress vs. Yesterday’s Sandcastle: Market Realities

The reality is, today's mortgage market is structurally far more resilient than it was in the run-up to 2008.

A significant portion of that $13.9 trillion in mortgage debt consists of "qualified mortgages" (QMs). These lending standards emerged directly from the ashes of the 2008 crisis, largely due to regulations like the Dodd-Frank Wall Street Reform and Consumer Protection Act and the work of the Consumer Financial Protection Bureau (CFPB).

These rules are specifically designed to help confirm that borrowers actually possess the ability to repay their loans. While not all outstanding debt falls under QM rules (many pre-date them), the vast majority of new originations do.

Homeowner equity reached a record $32 trillion in the first quarter of 2025. Many homeowners refinanced or purchased properties with historically low interest rates, locking in predictable, manageable payments.

This creates a substantial financial buffer. Property values could decline, and many homeowners wouldn't even find themselves underwater on their mortgages, let alone be forced into a distressed sale.

It is considerably more difficult to over-leverage in real estate now than it was before 2008. The guardrails are significantly tighter now; the anything-goes lending environment of the mid-2000s is largely a thing of the past.

Does this mean real estate prices are immune to declines? Absolutely not. Analysis has shown overbuilding and price sensitivity in certain markets; for instance, places like Austin, Texas, and parts of Florida have experienced price corrections and increased inventory through early 2025, reflecting localized supply dynamics.

Conversely, other markets, sometimes those supposedly being abandoned, have seen prices hold firm or even appreciate. Real estate is, and always will be, intensely local.

"The housing bubble burst because of a failure in both lending practices and regulatory oversight, which wealth managers must always keep in mind when assessing risk."

Mohamed El-Erian Chief Economic Adviser at Allianz

Analysis

So, what's the real game here? Why the panic if the data suggests a contained issue rather than a systemic threat? Part of it is pattern recognition – or misrecognition. The trauma of 2008 is seared into our collective financial psyche.

Any tremor in the housing market, any talk of "subprime," immediately triggers those old fears. The media understands this; fear sells. A headline predicting calm rarely gets the clicks that a doomsday prophecy does.

But your job, as a thinking investor or simply a concerned citizen, isn't to react to every echo. It's to discern the signal from the noise. The current FHA delinquency rate, around 6.8% as of Q1 2025, is a concern for those affected borrowers and for the FHA's insurance fund.

It signals that a segment of the population, often first-time homebuyers or those with fewer financial shock absorbers, is feeling the pressure from inflation, higher interest rates, or shifts in the job market. This is valuable information. It’s a data point about economic health at a specific stratum.

However, it's not necessarily a harbinger of doom for the entire multi-trillion dollar housing market, especially when that segment is a relatively small component of the whole, and the broader structure is built on much firmer foundations than in 2007.

The leap from "some FHA borrowers are struggling" to "the entire housing market is about to implode like 2008" is a chasm too wide to cross without ignoring a mountain of countervailing evidence. The narrative that FHA loans are a primary catalyst for an imminent, 2008-style housing implosion appears disproportionate to the actual systemic risk they currently pose.

Final Thoughts

Do I believe we're on the precipice of another 2008-style subprime housing catastrophe triggered by FHA loans? Based on the current data and market structure, the answer is no. Could we face a different kind of economic turbulence? Perhaps something more akin to the 2000-2001 dot-com adjustment for certain sectors of the equity markets? That's a more plausible scenario and a conversation for another day.

This specific anxiety – that FHA loans are the fuse on a bomb set to devastate the housing market anew – seems to be a narrative that grabs attention but wilts under careful scrutiny of scale and context. Your strategic imperative is to see through the fog of fear-mongering. You need to be a critical thinker, driven by data, not by drama.

When you encounter a frightening headline, especially one that invokes the ghost of 2008, dig. Who is saying it? Is it a balanced news report or an opinion piece with an agenda? What data are they actually presenting, and, more importantly, what are they omitting? Understand scale. A percentage increase in a small number remains a small number in absolute terms. A problem in one component of a complex system doesn't automatically mean the entire system is compromised.

Focus on fundamentals. Examine the broader economic picture, the current regulatory frameworks, and the true structural integrity of the market in question. Emotions are notoriously poor investment counselors. Panic might sell newspapers and generate clicks, but data and clear-headed analysis build and protect wealth.

The objective isn't to react to every market rumor or media-stoked fear. It's about understanding where genuine threats lie and where opportunities might be concealed when the crowd is stampeding in the wrong direction. The market is always shifting, but clear thinking and a firm grasp of the facts are your best defense. Keep your head. Keep your wits about you. And question everything.

Did You Know?

The Federal Housing Administration (FHA) was established by the National Housing Act of 1934. Its creation was a direct response to the banking crisis of the 1930s, aiming to stabilize the housing market and increase homeownership by providing mortgage insurance to lenders, thereby reducing their risk.

Disclaimer: The information provided in this article is for general informational purposes only and does not constitute financial, investment, legal, or tax advice. It is essential to conduct your own research and consult with qualified professionals before making any financial decisions. The author and publisher are not responsible for any actions taken based on the content of this article. Market conditions can change rapidly, and past performance is not indicative of future results.